India’s cement industry is a major energy consumer. This sector is undergoing a significant shift towards sustainability. Leading players have ambitious net zero targets for 2050.

Renewable energy (RE) is central to this decarbonization journey. The three largest cement manufacturers of India by manufacturing capacity (Ultratech, Shree Cement, Dalmia) are all members of the RE100. They have installed over 1800 MW of RE capacity, split between waste heat recovery systems (WHRS) and solar/wind power.

Grinding units face distinct challenges and opportunities. They purchase expensive grid electricity, making RE a lucrative option. However, energy storage systems (ESS) are crucial to meet round-the-clock demands due to the absence of captive power plants (CPP).

Integrated units, with energy-intensive clinkerization, primarily rely on thermal CPPs. This complicates their green transition. Yet, innovations like electric rotary kilns promise a future with more RE integration.

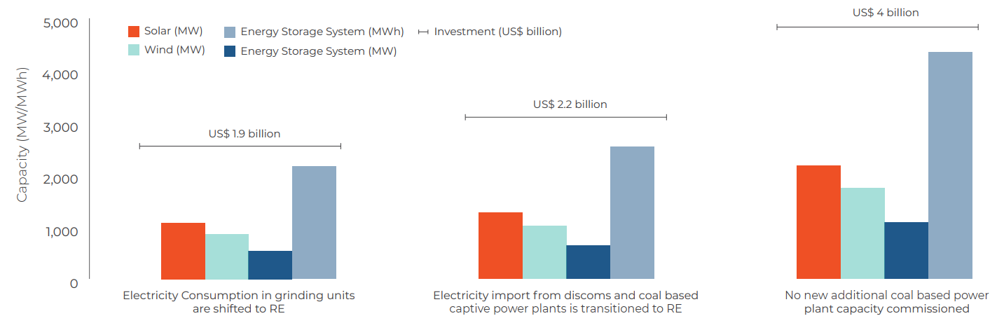

JMK Research predicts a 4-5 GW RE capacity increase by 2030 in the cement sector. This will demand over US$4 billion in investments, including ESS.

As the cement industry navigates this complex transition, it’s clear that a combination of policy support, technological innovation, and strategic investments will be crucial in driving the sector towards a sustainable future.

Reference- JMK Research report, Mercom India, Economic Times, Moneycontrol.com, Business Insider