India’s renewable energy (RE) landscape continues to evolve at scale. The March 2026 monthly update by JMK Research & Analytics presents a picture of steady growth, yet uneven delivery across segments.

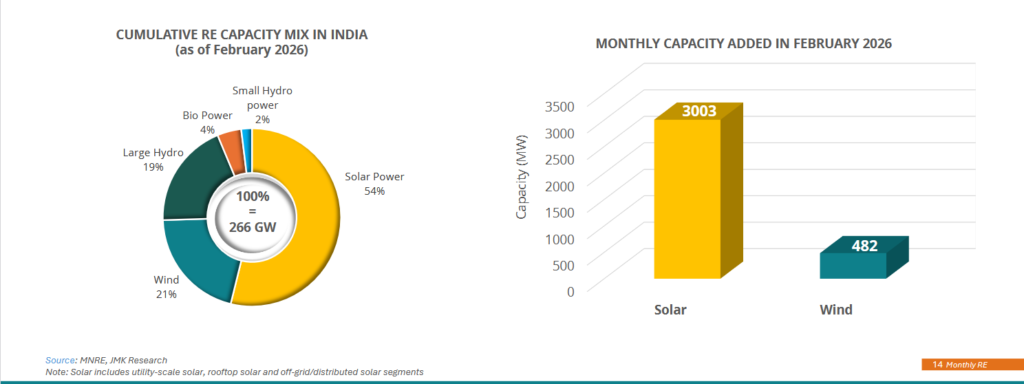

Total renewable capacity additions remained consistent during early 2026. Solar energy dominated new capacity additions, contributing the largest share month-on-month. Wind installations, though present, lagged behind solar in pace.

India’s cumulative renewable capacity has crossed 260 GW, reinforcing its position among the world’s leading clean energy markets. The report highlights that utility-scale solar continues to drive expansion due to falling tariffs and strong auction pipelines.

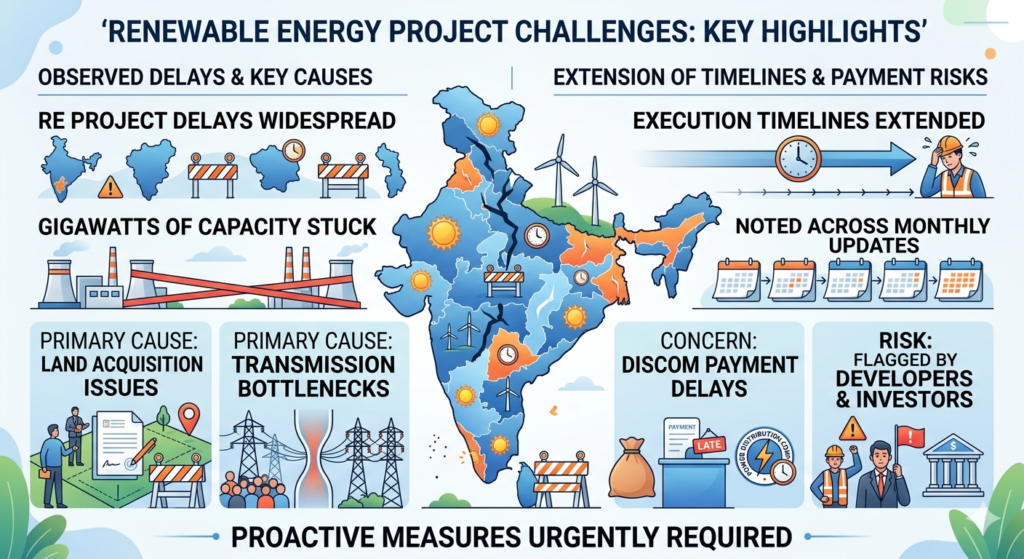

However, project delays were observed across several states. Multiple gigawatts of capacity stuck in various stages of development. Land acquisition issues and transmission bottlenecks were identified as primary causes.

Execution timelines continue to extend. Recent monthly updates consistently highlight this trend. Payment delays from distribution companies remain a concern. Developers and investors also flag these risks.

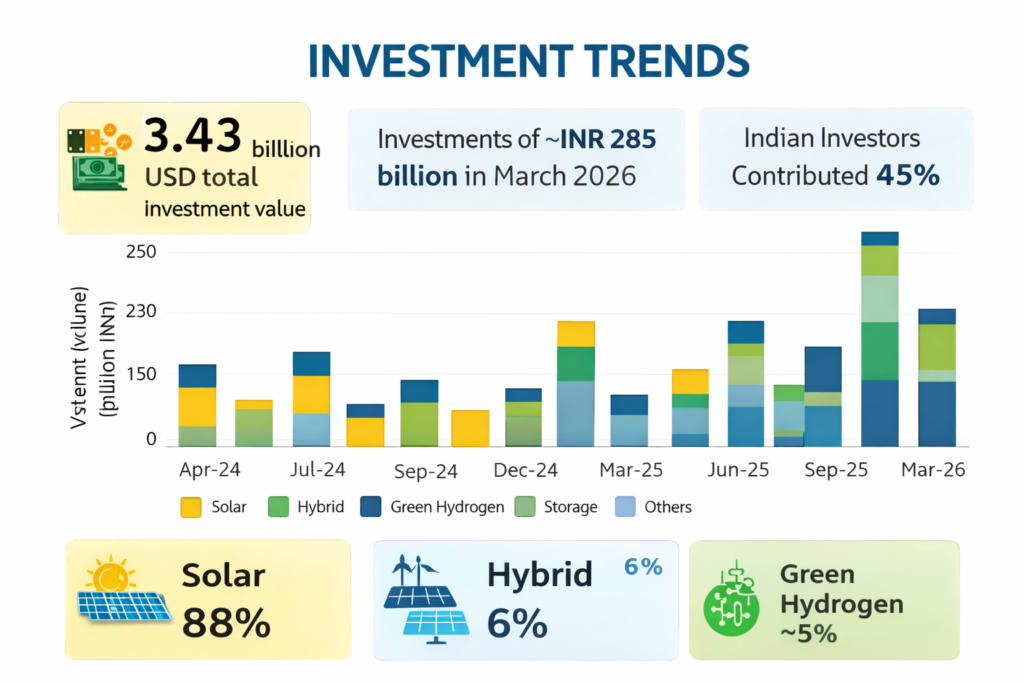

Investment activity, however, remains resilient. The investment trends indicates continued inflow into solar and hybrid projects. Both domestic and international investors are actively participating in India’s renewable expansion.

Battery storage is emerging as a critical enabler. The report notes increasing interest in hybrid and storage-linked projects. This shift reflects the growing need for grid stability as renewable penetration rises.

India’s long-term target remains ambitious. The country aims to achieve 500 GW of non-fossil capacity by 2030. Current trends suggest that while capacity addition is on track, execution efficiency must improve.

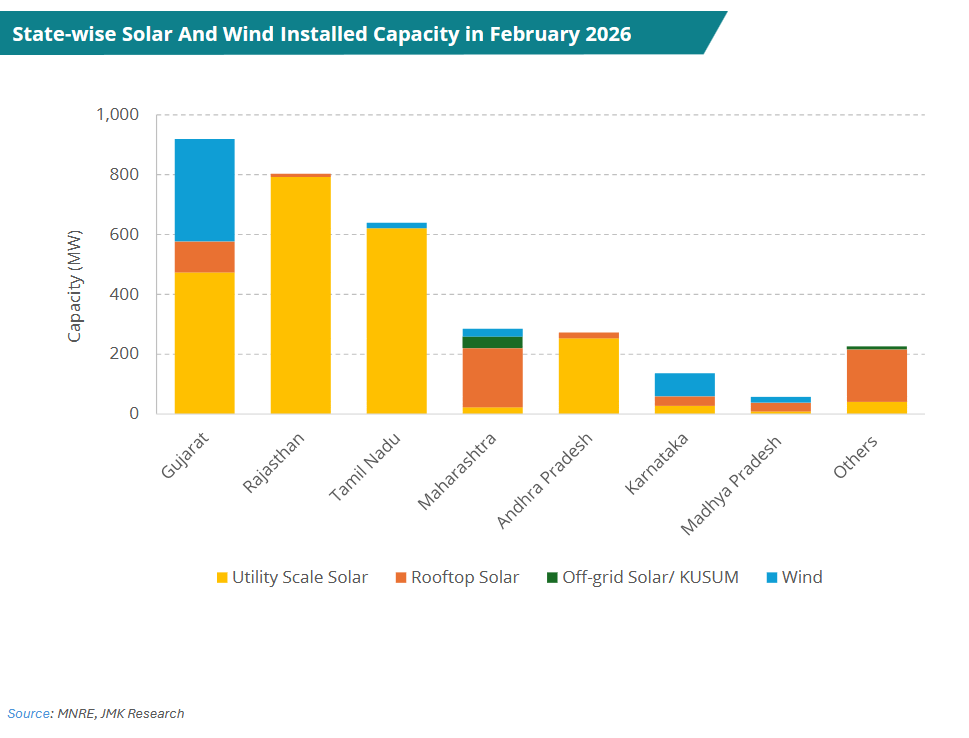

The state-wise installation map shows concentration in a few regions. Rajasthan, Gujarat, and Tamil Nadu continue to lead deployment. This geographic concentration raises concerns about grid balancing and regional disparities. Meanwhile, rooftop solar adoption remains slower than expected. Policy uncertainty and financing barriers have limited growth in this segment.

India’s renewable story is no longer about intent. It now depends on delivery at scale. The country is building the systems needed to support this transition. The growth is visible but the pace of progress will depend on how quickly bottlenecks are resolved.

Reference- JMK Research Monthly RE report, Wikipedia, MNRE website