India’s battery energy storage sector is growing fast. Yet the economics underpinning that growth are cracking.

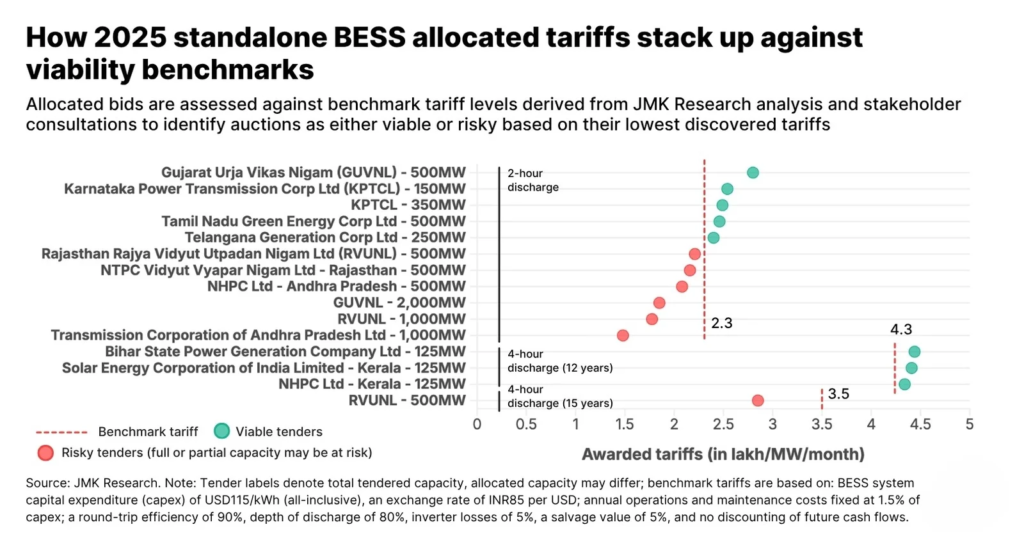

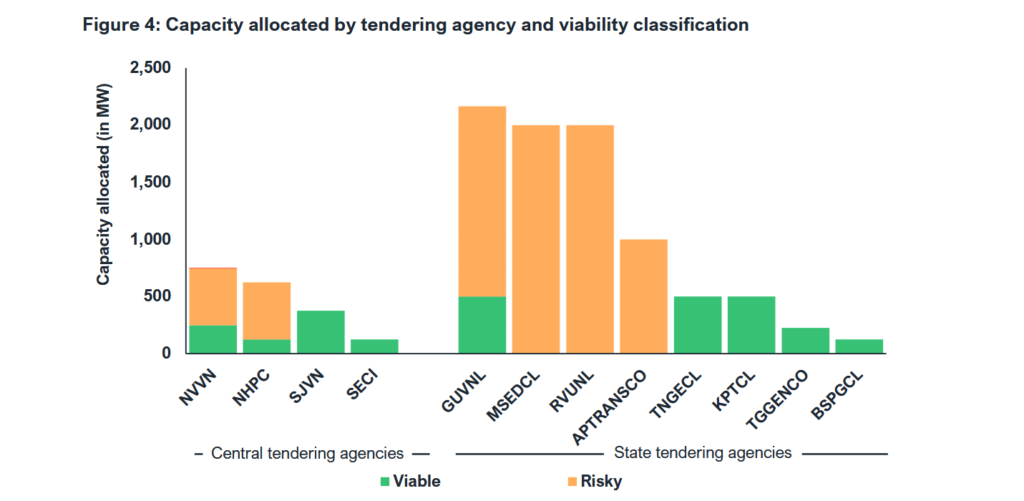

A joint report by JMK Research and the IEEFA, released in May 2026, reveals a deepening mismatch between tariffs awarded in 2025 auctions and actual project costs. Standalone battery energy storage system (BESS) tenders made up 60% of all energy storage capacity tendered in India in 2025. A total of 10.4 gigawatts (GW) of standalone BESS capacity was allocated across 18 tenders.

The numbers tell a troubling story.

The benchmark tariff for a standard 2-hour, 2-cycle BESS system stands at INR 2.3 lakh per megawatt per month (USD 2,449/MW/month). However, the lowest bids discovered fell to just INR 1.48 lakh/MW/month (USD 1,576/MW/month) — a 36% discount to viable levels. Consequently, nearly 75% of the 6,890MW allocated under this dominant configuration falls into the “at-risk” category.

The tariff crash is not proportionate to cost reductions. Between 2022 and 2025, average standalone BESS tariffs fell by 79.6%. Battery pack prices, by comparison, declined by only 36.5% during the same period, according to BloombergNEF data cited in the report.

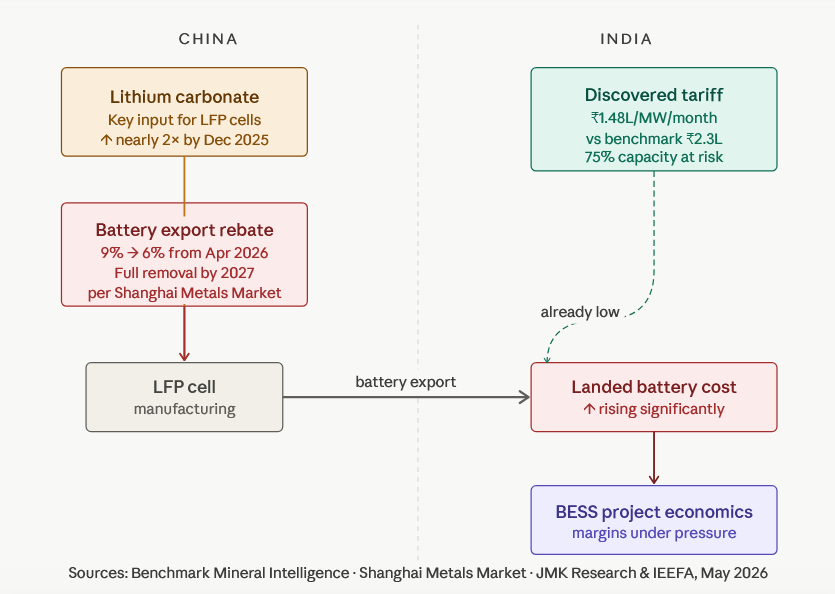

Supply chain risks are also adding pressure. For instance, Benchmark Mineral Intelligence said lithium carbonate prices in China nearly doubled by December 2025. Since lithium carbonate is a key raw material for lithium iron phosphate (LFP) cells, rising prices could significantly increase battery production costs.

China has also started reducing battery export rebates. The rebate fell from 9% to 6% in April 2026. Beijing plans to remove it fully by 2027. Analysts expect the move to increase India’s landed battery costs significantly.

Developer readiness is also uneven. Only 46.3% of allocated capacity went to developers with proven standalone BESS execution experience. The remaining capacity was awarded to entities with limited or no track record. Notably, some awardees are from unrelated sectors — food processing, mining, and packaging.

Financing conditions remain tight. Lenders expect internal rates of return (IRRs) of 15–20% for BESS projects, given high input cost variability and limited historical precedent.

The report calls for reforms. It recommends cost-reflective tariff floors. It also seeks stricter developer eligibility rules and standard payment security systems. In addition, it proposes a phased expansion of domestic cell manufacturing.

India’s domestic BESS capacity stood at just 1.8 gigawatt-hours (GWh) in March 2026. By comparison, China added 65GWh in December 2025 alone.

India targets 500GW of renewable energy by 2030. Whether BESS can deliver the storage backbone for that ambition depends entirely on whether tariff realities align with execution realities — and soon.

Reference- JMK Research & IEEFA, “Viability of Standalone Battery Energy Storage Tariffs Discovered in 2025” (May 2026); BloombergNEF; Benchmark Mineral Intelligence; Ember.