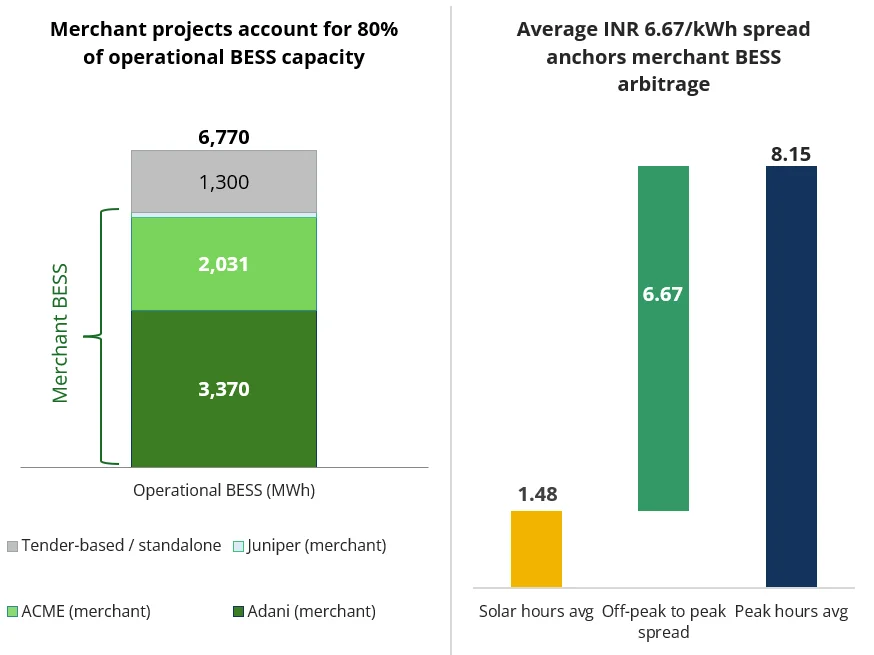

India’s battery energy storage system (BESS) sector grows fast. Merchant models now dominate. They account for 80% of the roughly 6.8 GWh operational capacity.

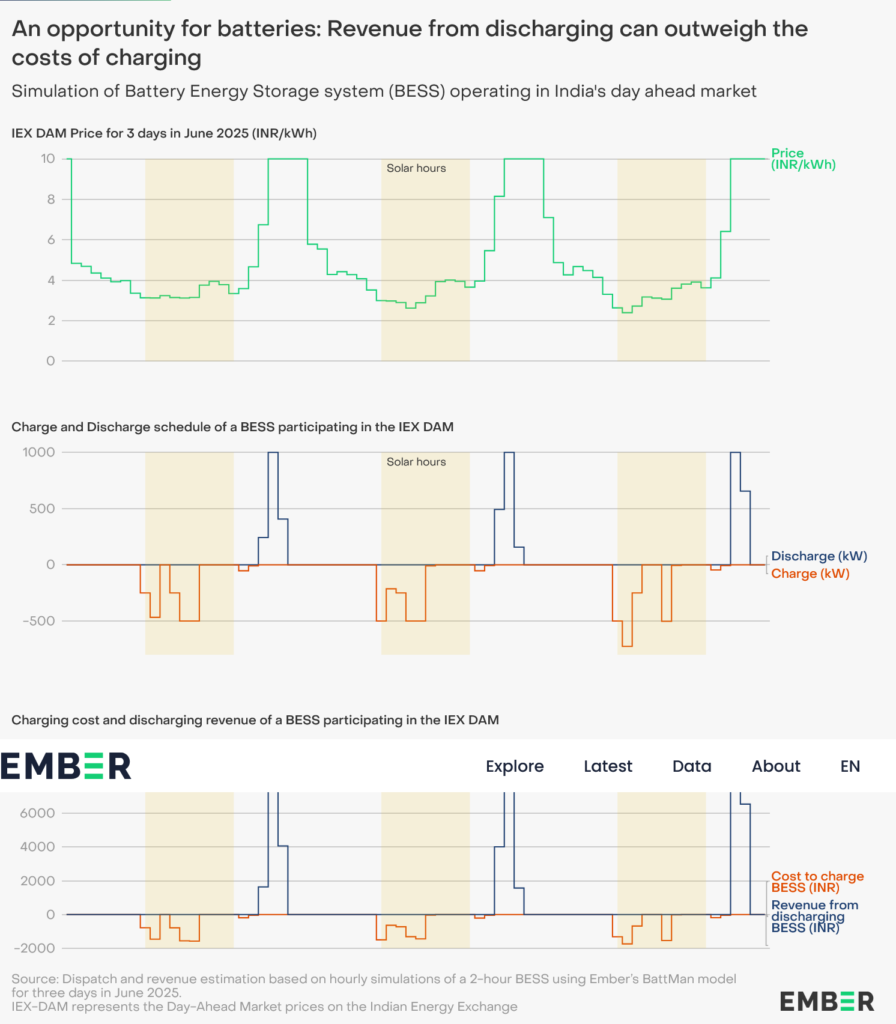

Large projects lead recent additions. Adani commissioned a 3,370 MWh system in Gujarat. ACME added 2,031 MWh in Rajasthan. These stand out in the merchant segment. Merchant batteries operate without long-term contracts. They charge at low prices and discharge at high prices. This model fits India’s power market well. Surplus solar often drives daytime prices near zero. Evening peaks push prices higher.

New draft rules test the model. Central and state measures restrict grid charging. They require paired renewable capacity for storage projects seeking ISTS connectivity. Rajasthan’s RVPN draft limits charging to co-located renewables only.

Experts highlight risks. A captive renewable mandate raises project capex by 60-80%. It adds land, approvals, and delays. Revenue suffers from limited arbitrage windows. SLDC discretion introduces uncertainty. Lenders may demand higher rates.

India crossed 50% non-fossil power capacity in 2025. The National Electricity Plan projects 47.24 GW/236.22 GWh BESS need by 2031-32.

Stakeholders push back. Blanket restrictions could slow deployment. Targeted measures are suggested. These include grid charging in surplus windows and clear congestion rules. The 45th CMETS-WR meeting showed some progress.

Merchant BESS became profitable in 2024 for the first time. Battery costs fell sharply. Market revenues rose. Ember analysis confirms this shift. IRRs up to 17-24% appear possible under right conditions.

Policy balance matters. India needs scalable storage. Overly rigid rules may raise financing costs and delay clean energy integration. Flexible frameworks can support grid stability while preserving merchant viability.

Reference- JMK Research, IEEFA, Business Standard, Ember